A new third pillar of retirement, the Finpension 3a, is here to help you save for your golden years. It’s an excellent new option that will give you peace of mind and a better quality of life in your old age.

The viac is an excellent new third pillar that allows you to invest in a private company.

(Affiliate links may be included in some of the links below.)

Finpension has recently launched 3a Finpension, its third pillar product. It’s also very fascinating.

Finpension is already behind valuepension, Switzerland’s finest vested benefits (second pillar) account. As a result, it’s fantastic that they’re now offering a third pillar account.

So, let’s take a closer look at 3a Finpension.

In this post, I’ll examine into many aspects of 3a Finpension, including their costs, investing plan, and security. Finally, I’ll evaluate it in comparison to other third-party suppliers.

You’ll also have a chance to win 6883 CHF in your third pillar if you use my coupon!

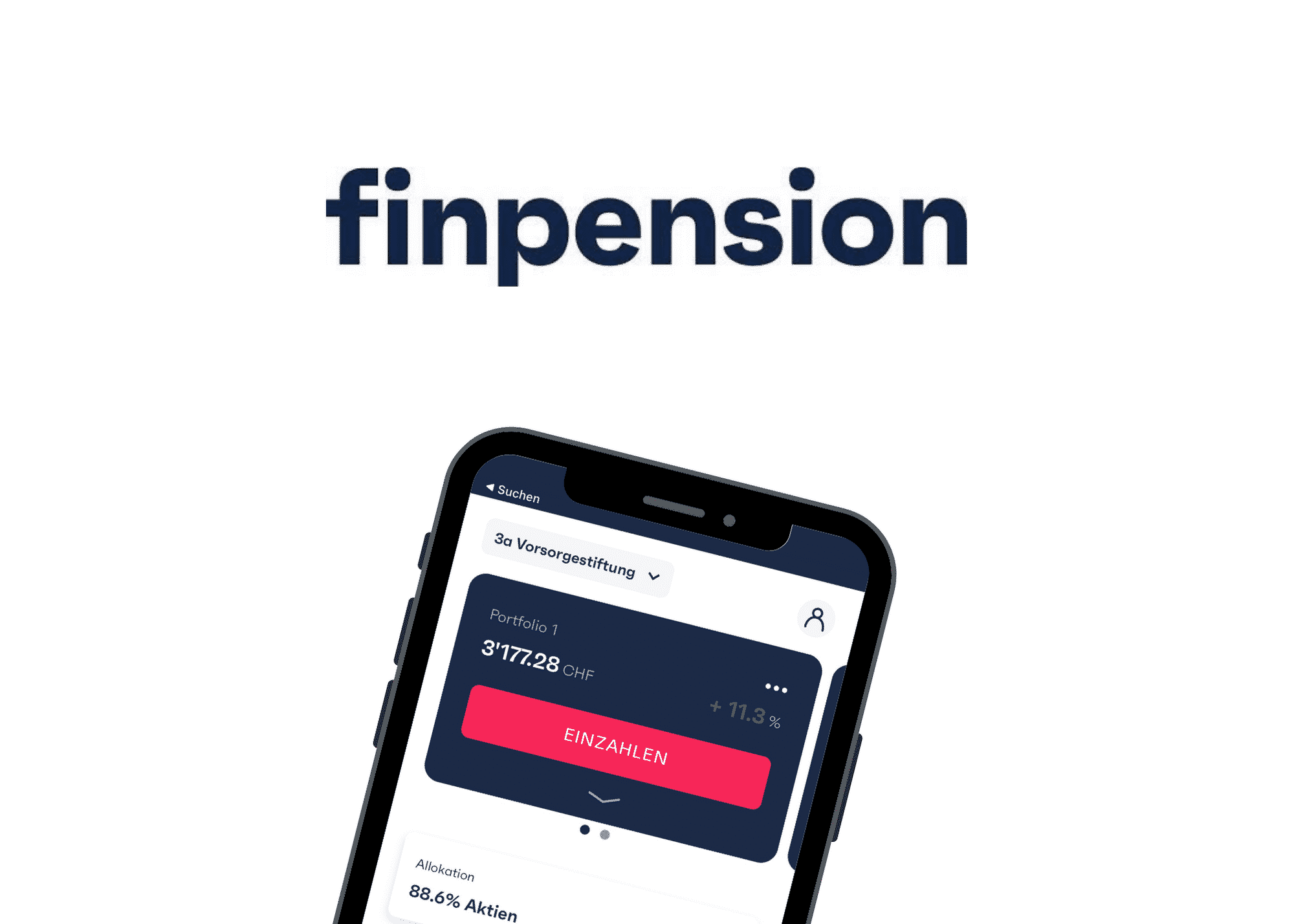

Finpension 3a

The most effective Third Pillar!

Finpension 3a

Finpension 3a is Switzerland’s finest third pillar.

In your third pillar*, enter the FEYKV5 code for a chance to win 6883 CHF!

* * * * * * (if you deposit 1000 CHF in the first 12 months)

![]()

Finpension 3a is a finpension AG-managed pension foundation. The third pillar product is linked to Finpension 3a. However, since 2017, finpension has handled additional types of pension assets, such as vested benefits, via their valuepension service.

Finpension began with the yourpension collective foundation, a pension solution for the second pillar’s non-mandatory portion. Customers like it so much that they wanted to retain their accounts when they retired. As a result, finpension began providing vested benefits (valuepension). Now, in 2024, they will begin their third pillar offering: finpension 3a.

It’s essential to remember that the foundation is distinct from the management firm. As a result, there is a clear separation of books for the assets.

The third pillar account may be accessed in two ways:

- On the App Store and Google Play Store, there is a mobile application.

- A browser-independent web application.

The fact that they also offer a web application is a huge plus for me.

If you’re interested in learning more, I spoke with the CEO of finpension.

Investment Methodologies

Finpension 3a is mostly concerned with stock market investment. They provide six alternative methods to achieve this goal:

- Equity in Finpension 0

- Equity Finpension 20

- Equity Finpension 40

- 60 % Finpension Equity

- 80 % Finpension Equity

- Finpension Equity is a 100-percent owned company.

The allocation to equities in the portfolio is represented by the number in the strategy. Bonds make up the remainder of the portfolio, with real estate accounting for 9%. However, each plan includes a 1% cash allocation. Finpension Equity 100, for example, is made up of 99 percent equities and 1% cash. 60 percent of Finpension Equity 60 is invested in stocks, 30% in bonds, 9% in real estate, and 1% in cash. Finpension Equity 0 has a 99 percent bond allocation and a 1% cash allocation.

You may also select from three other investment foci in addition to these strategies:

- A portfolio that is internationally diversified.

- Switzerland: A portfolio with a primary emphasis on Swiss stocks.

- Sustainable: A portfolio that exclusively invests in businesses that are committed to environmental, social, and governance (ESG) objectives.

As a result, you have a total of 18 tactics to select from. Everyone should be able to get enough! If the suggested approach does not meet your needs, you may devise your own. You’ll be able to choose from a wide variety of index funds for this.

Finpension 3a invests in index funds rather than exchange traded funds (ETFs). From the viewpoint of a pension foundation, there are many benefits to doing so:

- They are entitled to a refund of withholding taxes on profits received from overseas stocks.

- When opposed to ETFs, these funds have no stamp duty to pay.

- They have access to very low-cost funds that are usually only available to institutional investors.

They put their money into Credit Suisse institutional funds, which are big, efficient, and cost-effective.

All of the techniques are well-described on the website. You can discover which index funds each strategy invests in by looking at the table below. Here’s how the finpension equity 100 approach works:

Finpension 3a: Global Equity 100 Investing Strategy Finpension 3a: Global Equity 100 Investing Strategy Finpension 3a: Global

Finpension 3a: Global Equity 100 Investing Strategy Finpension 3a: Global Equity 100 Investing Strategy Finpension 3a: Global

This approach includes a fair mix of Swiss and international stocks. It also offers a nice mix of small and big capitalization stocks. I would spend less money if I were doing it personally, but this approach should work for most people.

Keep in mind that Finpension 3a cannot be uninvested in. You can’t have a bank account that’s entirely made up of cash. If you don’t want to put 99 percent of your money into stocks, you’ll have to go with bonds. The issue is that Swiss and European bonds now have negative yields. As a result, they are a less profitable investment than cash. This situation may change in the future, but for now, it is as it is. As a result, bond-investment techniques aren’t very good.

The mobile application allows you to create your own unique strategy. It’s simple, and you have very few restrictions on what you may accomplish. You may put 99 percent of your money into a World index fund (excluding CH) and have a very basic, well-diversified portfolio. And it will be a very low-cost portfolio! One of your limitations is that you can’t invest too much in a single stock. You’ll be restricted from investing in Swiss stock market indexes that are highly weighted in three major corporations.

It’s worth noting that none of their plans contain more than 1% cash. A cash third pillar account is not possible. You may utilize a money market fund if you select a bespoke strategy. As a result, you’ll be able to primarily invest in stocks, bonds, real estate, and alternative investments (currently only gold).

Finpension 3a buys shares of the funds on the first banking day of the month with the money in your account (after a deposit). And if you wish to switch strategies (for free! ), Finpension 3a will do so on the first banking day of the week.

Once a week, on the first banking day of the week, your portfolio will be rebalanced. If the allocation deviates by more than one percentage point, rebalancing occurs.

Overall, the finpension 3a accounts’ investment methods are fantastic! I’m not sure what I have to say about it. They have a good stock allocation, good diversity, and a good flexibility to modify the portfolio. Furthermore, they do not impose currency hedging on you, which is a fantastic feature.

If you don’t want to put 99 percent of your money into equities, you’ll have to invest in negative-yielding bonds. So, these accounts are excellent for individuals who invest 99 percent of their money in stocks, but not so much for people who invest a lesser percentage of their money in equities.

Fees for Finpension 3a

Let’s look at the costs associated with investing with finpension 3a now that we’ve examined their investment plans.

Finpension’s costs are based on a fixed rate. Without VAT, this flat rate is set at 0.39 percent. This flat rate is 0.42 percent, based on a VAT of 7.7%. As a result, the basic charge will be 0.42 percent. The marketing charge of 0.39 percent is the figure.

You will also be responsible for the product expenses. These expenses vary depending on the approach you choose. Fortunately, finpension is a Credit Suisse institutional customer. Some of the index funds have no costs for institutional customers. As a result, the majority of the funds will have no costs. There are certain exceptions, such as Real Estate and Emerging Markets funds. Even yet, the costs for these exclusions are extremely modest.

The finpension Equity 100 strategy, for example, has product expenses of 0.02 percent. Even better, if you create a bespoke approach, you can achieve product costs of 0.00 percent!

Finpension 3a has a zero TER for a bespoke strategy.

Finpension 3a has a zero TER for a bespoke strategy.

So, using the Equity 100 plan (the greatest long-term approach), your total expenses each year will be 0.44 percent! This price is extremely inexpensive, costing 10% less than the lowest option! You can even go to 0.42 percent if you employ a bespoke approach!

And that’s all there is to it! On foreign currency transactions, Finpension does not charge a margin. However, the bank they are using has a 0.05 percent currency conversion spread. Importantly, the majority of their assets are held in CHF, and there are no load or redemption costs. However, certain mutual funds offer minimal load and redemption costs (below 0.10 percent ).

Finally, you’ll be able to save money on fees! You will get a fee credit of 25 CHF if you refer Finpension 3a to someone who actively utilizes it. This implies that for each person you invite, you will save 25 CHF, and there is no limit to the number of people you may invite. You can even win a year of third pillar donation if you apply my code (in the following section).

Overall, the Finpension 3a account’s costs are great! All of their fees are at least as excellent as, if not better than, the lowest third pillar in Switzerland. Finpension 3a account is the cheapest third pillar account for individuals who wish to invest in equities aggressively!

If you withdraw money from the third pillar early, you’ll have to pay a few additional fees.

You will have to pay 250 CHF if you make an early withdrawal for a home. Finpension charges 200 CHF if you pledge your third pillar for a real estate property.

You must pay 150 CHF if you transfer your Finpension 3a assets within one year of opening your account.

Finally, if you remove your assets while in Switzerland, you will be charged 750 CHF during your first year at Finpension and 250 CHF after that.

These costs are less important since they are unusual and unrelated to investments. However, if you believe you will fall into one of these groups, you should consider them.

Register for a Finpension 3a account.

You may win 6’883 CHF if you use my code FEYKV5 throughout the procedure (if you transfer or deposit CHF 1000 during the first 12 months).

The process of opening a Finpension 3a account is simple and takes just a few minutes. Open your phone, browse to your preferred app store, and download the finpension app, then follow the steps.

They’ll start by asking for your phone number and an account password. Then, depending on your age, they’ll calculate your investment horizon.

Finpension 3a has a long-term investment horizon for me.

Finpension 3a has a long-term investment horizon for me.

Following that, you’ll be asked a series of questions regarding your risk tolerance. And they’ll utilize that information to help you select an investing plan. You may, however, pick your own approach if you don’t like the one provided. Don’t worry, you can always alter it afterwards.

Finpension 3a’s risk tolerance

Finpension 3a’s risk tolerance

After you’ve decided on a strategy, all you have to do now is fill in your personal information, and you’re done! Your account is already set up to accept a deposit. It’s silky smooth.

You may also build up to five portfolios per individual, which is fantastic. It implies you may make staggered withdrawals to reduce your tax liability. Read my post on the third pillar for additional details on this optimization.

Security

It is essential to examine the security of each institution if you want your money to endure a long period.

Let’s start with the Finpension 3a application’s technological security. All data sent between the application and the servers is encrypted. You’ll be given a phone number and a password to connect with.

For your account, you may opt to enable a second factor of authentication. This will use SMS authentication to link your account to your phone number. This gives your account an extra degree of protection.

Also, while establishing an account, I would like to have a complete identity check.

Your funds will be kept at the finpension 3a foundation’s custodian bank. Credit Suisse is the current custodian bank. Swiss law protects this money up to 100,000 CHF. This should not be a problem since Finpension 3a strategies have very little cash.

Your securities are held in Credit Suisse’s institutional funds, which manage over 100 billion CHF in pension assets. It is preferable to have a big management rather than a tiny unknown bank.

The foundation’s financial statement includes all of the money. On its financial sheet, this foundation solely contains client assets. The money are secure with the foundation even if finpension (the asset managers) goes bankrupt. In addition, the foundation will need to hire a new executive director.

Overall, I believe the Finpension 3a provides enough security. The foundation’s separation from the asset management firm is a good thing in terms of security.

VIAC versus Finpension 3a

Until recently, I’ve always promoted VIAC as Switzerland’s finest third pillar. Let’s examine how Finpension 3a stacks up against VIAC. Is it Switzerland’s new best third-pillar account?

Let’s begin with the costs. Finpension 3a costs 0.44 percent (0.42 percent with bespoke strategy) less than VIAC, which costs 0.45 percent. There isn’t much of a distinction here.

Furthermore, Finpension has a very modest currency conversion spread (0.05 percent), while VIAC has a big one (0.75 percent ). Now, it’s true that VIAC uses netting to lower that cost. With netting, it cost less than 0.25 percent in practice. Furthermore, a large number of funds are held in CHF, making it less expensive. It’s also a one-time expense. Finpension 3a, however, is still less expensive.

Finpension 3a allows you to invest up to 99 percent in equities, while VIAC only allows you to invest up to 97 percent. Again, it’s not a significant difference, but it will mount up over time.

When developing a bespoke strategy using finpension 3a, you also have greater flexibility than with VIAC. Finpension 3a, for example, allows you to build a portfolio with a 99 percent foreign currency exposure, while VIAC only allows you to create a portfolio with a 60 percent foreign currency exposure! This function is ideal for investors that have specific requirements.

VIAC may be a better option than Finpension 3a if you do not want to have 99 percent of your money invested in equities. They do, in fact, allow you to invest in cash. Finpension 3a requires you to invest in negative-yielding bonds, which may not be the best option. As a result, VIAC may be preferable if you have a modest stock allocation.

A smartphone application and a web application are available for both VIAC and Finpension. As a result, they are both very useful.

Both services seem to be completely open and trustworthy. They both provide a high degree of security and protection for your valuables. Finally, they both have an excellent reputation.

Finpension 3a is a superior third pillar than VIAC because of its greater stock allocation and cheaper fees. As a result, Finpension 3a is now Switzerland’s best third pillar! VIAC, on the other hand, is just somewhat inferior and still a fantastic choice.

VIAC is perhaps still preferable for individuals who do not wish to be completely engaged in equities. Investing in negative-yielding bonds does not make sense right now. However, if you have a lengthy investment horizon, you should consider investing entirely in equities.

I have a full post on VIAC versus Finpension 3a if you want more information.

Pros of Finpension 3a

Let’s briefly go through the benefits of Finpension 3a:

- Fees are very cheap!

- Stocks allow you to invest up to 99 percent of your income.

- The investors are not compelled to hedge their currency positions.

- The registration procedure is simple.

- With a lot of flexibility, you can design your own investment plan.

- There are no restrictions on foreign investments.

- There are no restrictions on the use of foreign currencies.

- On their website, they provide excellent openness about all money and costs.

- You have the option of creating up to five portfolios.

- Apps for smartphones and the web

3a Finpension Cons

Let’s briefly go through the drawbacks of Finpension 3a:

- Finpension is a brand-new product.

- During the account creation process, the identity of the user is not confirmed.

- Negative-yielding bonds are a good investment.

- The mobile application does not support two-factor authentication.

These drawbacks are minimal.

Conclusion

The most effective Third Pillar!

Finpension 3a

Finpension 3a is Switzerland’s finest third pillar.

In your third pillar*, enter the FEYKV5 code for a chance to win 6883 CHF!

* * * * * * (if you deposit 1000 CHF in the first 12 months)

Finpension delivered on my expectations for a solid third pillar account, and I was not disappointed. Finpension 3a is a fantastic third-pillar account. It is now Switzerland’s best third pillar (for people investing fully in stocks).

With the suggested methods, the fees are extremely minimal, with a minimum of 0.44 percent. With a unique approach, you can even go to 0.42 percent. The entire price structure is also extremely beneficial.

You may also invest up to 99 percent of your income in equities. You may have an exceptionally well-diversified portfolio with just one or two funds if you use a bespoke approach.

Finpension 3a is thus superior than VIAC! My portfolios are presently being transferred from VIAC to Finpension 3a. I plan to transfer all of my accounts before the end of 2024. In 2024, I’ll start a new one at Finpension 3a.

Finpension 3a is really worse than VIAC in one aspect. If you don’t want to put all of your money into equities, VIAC may be a better option. Finpension will require you to invest in negative-yielding bonds. You may invest in cash (with a 0.1 percent return) at VIAC, which is presently a better option than bonds. And with VIAC, you’ll only have to pay fees on the money you’ve put in.

Finpension 3a, on the other hand, is presently superior than VIAC for aggressive investors like myself.

If you create a Finpension 3a account with my code FEYKV5, you’ll be entered to win 6883 CHF!

If you like this article, check out my evaluation of the finpension vested benefits offer – valuepension.

What are your thoughts on Finpension 3a’s new account?

Directly to your email, we’ll provide you our finest tactics and suggestions.

Get free personal financial advice that can help you achieve Financial Independence!

The author of thepoorswiss.com is Mr. The Poor Swiss. He recognized he was slipping into the lifestyle inflation trap in 2017. He made the decision to reduce his expenditures while increasing his income. This blog chronicles his journey and discoveries. In 2019, he plans to save more than half of his salary. He set a goal for himself to achieve financial independence. Here’s where you may send a message to Mr. The Poor Swiss.

Related Tag

- third pillar bank or insurance